What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 11/15/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+2.6

|

+120%

|

|

Bloomberg Galaxy Crypto Index

|

+1.1%

|

+127%

|

|

S&P 500

|

+2.1%

|

+11%

|

|

Gold (XAU)

|

-1.1%

|

+23%

|

|

Oil (Brent)

|

+8%

|

-34%

|

Source: TradingView, CNBC, Bloomberg

The Equity Markets Were Vaccinated - Sector Rotations

No matter how many times we wrote/said that risk assets would rally as soon as the election ended, it still triggers a double-take every time we look at the almost comical MTD returns of risk assets (S&P +8%, Oil +8%, BTC +16%, DeFi tokens +37%).

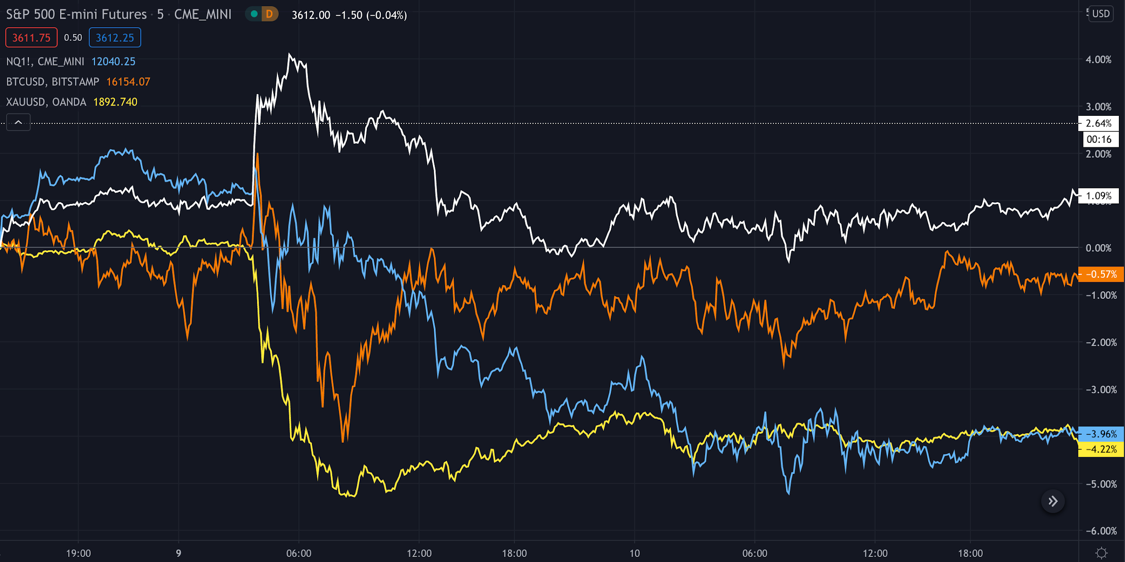

Let’s start with the equity markets, which saw $44.5 billion of inflows into US stock funds last week, the largest weekly haul by equity funds since EPFR began collecting the data, and the second-biggest inflow by US stock funds since 2000. The positive vaccine news certainly influenced this capital rotation, but the trend had been higher all month regardless. The vaccine announcement did, however, have a large and direct impact on sector rotations. Cyclical stocks and financials that have been negatively impacted by the pandemic and are thus more sensitive to the reopening of the economy outperformed last week, while sectors that have benefited from the pandemic underperformed (“COVID stocks” like Peloton, Zoom and Netflix were hit particularly hard). As you’d expect, we also saw a sharp sell-off in gold and treasuries. Interestingly, upon the news of Pfizer’s vaccine, the knee-jerk reaction was to send Bitcoin higher, but Bitcoin very quickly reversed course and actually moved substantially lower thereafter before recovering back to mostly unchanged. Other digital assets also fell briefly, many of which are essentially just early stage technology companies using a new type of instrument to bootstrap their growth and reward customers (pass-thru tokens). The overnight price reactions to the Covid vaccine illustrate these moves clearly, with the Nasdaq selling off sharply along with Gold, while the S&P initially spiked to record highs. Bitcoin, as it usually does, simply forged its own path.

S&P (white), Nasdaq (blue), Bitcoin (Orange) & Gold (yellow) all reacted rationally to the vaccine news

Source: TradingView

For those of us growing tired of markets that react almost entirely to Central Bank news, it was quite refreshing to see a rational market reaction that had nothing to do with the Fed. But it is worth noting that Bitcoin’s up, down, up again reaction shows that there is still confusion as to whether Bitcoin is a risk asset or a safe haven.

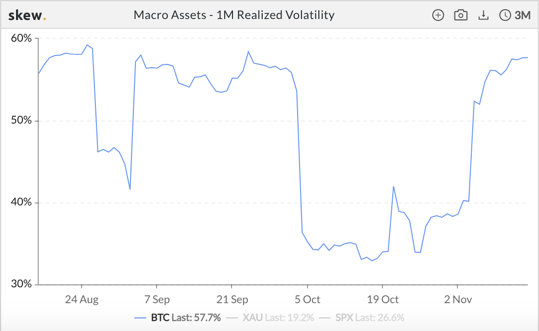

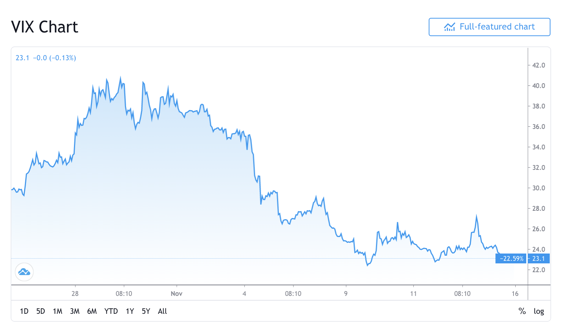

Perhaps even more interesting has been the effect on volatility markets. As our friends at Kraken pointed out, the VIX has fallen -35% in the past 2 weeks while Bitcoin's volatility has gained close to +20 percentage points.

|

Bitcoin 1-month Volatility

Source: Skew

|

Decline in the VIX

Source: TradingView

|

Drunkenmiller, Bill Miller, Ray Dalio and PayPal Spark Yet Another Bitcoin Rally

While Bitcoin acted as a “safe” asset immediately following Pfizer’s news, it quickly went back to being an oft-talked about risk asset by the end of the week. Bill Miller (very bullish) and Stan Druckenmiller (cautiously bullish) weighed in from the long side. Ray Dalio, meanwhile, warned that governments might ban Bitcoin should it become material (a view that we have refuted in the past, citing evidence that the US Government doesn’t normally auction off assets that they plan on banning).

While Drunkenmiller is perhaps the sexiest name of the recent Bitcoin advocates, we ascribe more value to Bill Miller’s words. Miller has used the same successful playbook for decades -- picking beaten-down securities that trade at a large discount to their intrinsic value. While his fund produced large returns in 2019 as a result of buying Bitcoin at distressed levels, for him to still find value near all-time-highs should give investors comfort that there is immense value here. Further, Bill Miller is more likely than Drunkenmiller, Tudor Jones or other macro traders to expand beyond Bitcoin into other areas of digital assets, once he (and other value investors) recognize that this “non-Bitcoin” token universe of cash-flow producing companies and projects even exists. Miller is a value investor, and the digital assets space has evolved beyond just “cryptocurrencies” to value-accruing pass-through and asset-backed instruments. These tokens issued by Decentralized Finance projects, as well as from sports, entertainment and gaming companies, accrue economic value from real cash flow generation and yields and will eventually attract more value investors like Miller.

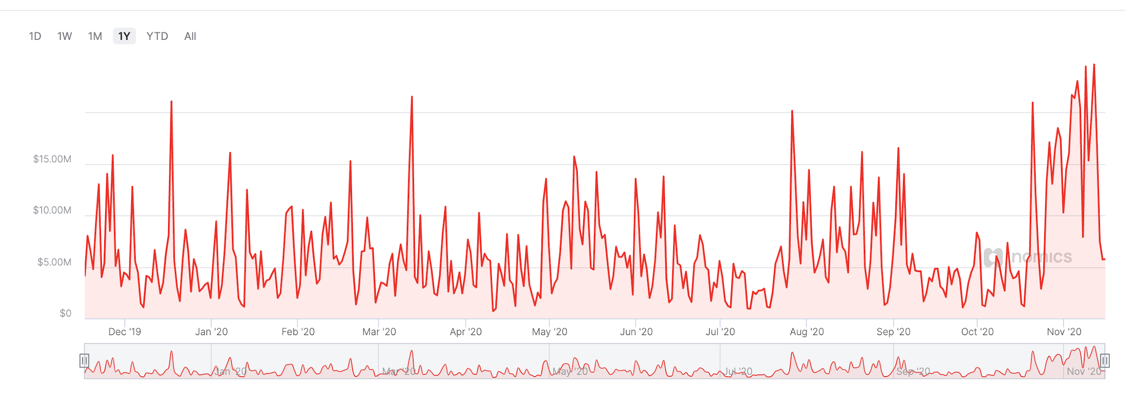

Beyond well respected hedge fund managers, we also saw further interest from the sell-side, as both Citi (calling for $310,000 BTC price) and JP Morgan (Bitcoin more attractive than gold) entered the public narrative. We’ve also personally received calls from multiple 2nd and 3rd tier investment banks, as broker/dealers are finally trying to figure out how to capitalize on an industry that has thus far left them behind (more on the “investment banking” opportunities next week). Retail investors were also flocking to digital assets last week via PayPal’s new interface. To illustrate the PayPal effect, one can track trading volumes on ItBit’s exchange, which is owned by Paxos, the liquidity provider chosen by PayPal for its digital assets business. Volumes on ItBit have spiked from $3-5 million per day to upwards of $20 million per day since the product rollout (which has only reached 10% of PayPal’s customers to date). Futher evidence of the PayPal effect can be seen in the advancements of lesser known cryptocurrency, Litecoin (LTC), a project that anyone in the digital assets space will tell you has no value whatsoever, but the token nevertheless jumped 17% last week and is +25% MTD.

Needless to say, there was a lot of interest in Bitcoin and digital assets last week.

Bitcoin Trading Volume on ItBit exchange, which powers PayPal

ESPN should issue a token

Every company will eventually have a token in its capital structure. Right now, token issuances are largely coming from projects within the digital assets industry, since their customers already understand how to own and send tokens. But soon enough, due to onramps into digital assets from PayPal and others, every person will understand how to own and utilize a token, and once they do, it will lead to a floodgate of issuance from creative and innovative companies.

Here’s how it could work. A company issues a token to its customers with dual-features (part utility / part “quasi-equity”). The utility is flexible at management’s discretion similar to loyalty rewards or discounts (i.e. airline miles or Amazon prime), and the “quasi-equity” takes the form of traditional dividends, buybacks, or token price growth mechanisms. Tokenholders are therefore both customers and stakeholders, leading to rapid growth of customers as each tokenholder becomes an incentivized evangelist.

Who better to try this than ESPN? According to Axios, their business model is dying as fans go direct to the source instead of to ESPN:

Cable TV is dying a slow death, and after years of mostly denying that reality, America's major media companies are beginning to hedge their bets and prepare for what comes next.

- 25 million homes have cut the cord since 2012, and another 25 million are expected to do so by 2025.

- If projections hold and the number of households with traditional pay-TV bundles stabilizes at ~50 million, U.S. media companies would lose ~$25 billion in subscription revenue, plus any advertising losses

- Partly due to the loss of live sports, the COVID-19 pandemic will drive cable and satellite TV providers to lose the most subscribers ever.

- This has created a "tectonic shift" in the industry, with Disney, NBCUniversal, WarnerMedia and ViacomCBS all announcing major reorganizations in the last four months with an eye towards streaming.

- Cable TV customers pay ESPN more than $9 per month, so the company has long been hesitant to cannibalize that deal by pivoting to streaming. But as cable subscriber numbers plummet, they clearly see the writing on the wall.

- In the last two weeks, ESPN laid off 300 people — many of them in TV production — and moved most of its premium written content behind the ESPN+ paywall in an attempt to drive subscriptions.

ESPN is insanely profitable -- for Disney shareholders. But ESPN customers share in none of this financial upside, and therefore customer stickiness is low. This is a similar dynamic to Amazon shareholders versus Amazon Prime members, where shareholders benefit financially while Prime members benefit only via utility of the service. The difference is Amazon Prime customers are happy and the benefits are increasing, while ESPN customers are not happy and the benefits are shrinking. ESPN could keep its cable relationships for older customers, while going direct to consumers with a token offering for younger customers. This token could have limited supply, creating scarcity value and upward price momentum as new customers want to own the token, as ownership of the token could unlock features exclusive to ESPN (premium content, access to players, etc). By pre-selling tokens to customers, ESPN’s revenue and balance sheet would grow (booking prepaid revenue upfront), which would allow ESPN to continue to compete for content and exclusive sports rights even as ESPN loses leverage with cable providers who want to pay less for a declining service.

30 years ago, a kid growing up in Dallas was a Mavericks fan and watched SportsCenter to catch up on the latest news and highlights. When NFL Sunday arrived, he watched the Cowboys on the living room TV.

Nowadays, a kid growing up in Dallas is still a Mavericks fan, but he's likely an even bigger fan of Luka Dončić, who he follows on Instagram (and who has almost 3x as many followers as the Mavs). He gets his news from social media, so there's no need for SportsCenter. When NFL Sunday arrives, he streams NFL RedZone, while watching his favorite player's latest YouTube vlog on his phone.

As direct-to-consumer grows, ESPN and other large aggregators will need a way to compete. Aligning customers and “shareholders” is one way to do this. Bill Simmons recently sold his “The Ringer” website and podcast network to Spotify for what is rumored to be over $200 million, but only Simmons and a small handful of equity investors benefited from this financially. Meanwhile, the Ringer’s employees are revolting and the customers who made the Ringer possible got nothing. Imagine the possibilities had the Ringer “decentralized” ownership via a token, where customers, employees and management all benefitted? That’s where we’re headed.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency