What happened this week in the Crypto markets?

Another 10-20% flash crash in crypto

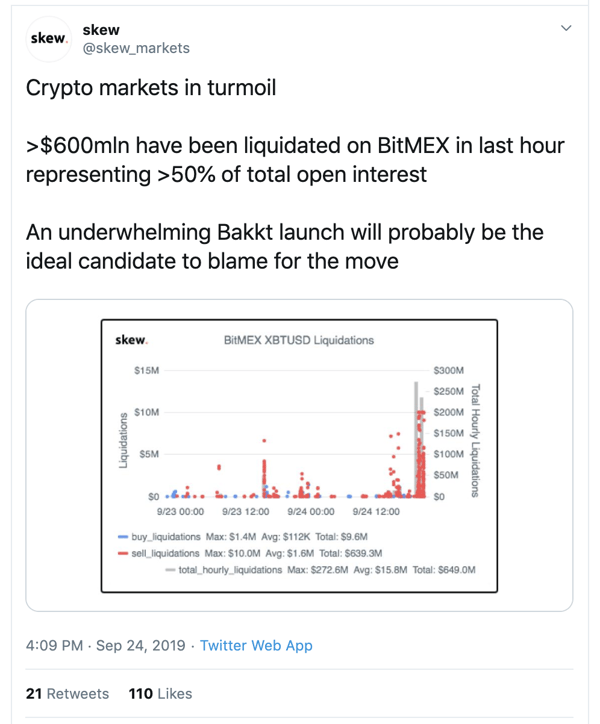

The crypto markets seemed stable for most of September, if not outright healthy. That all changed in a single 1-hour period on Tuesday when prices across the digital assets ecosystem had a crypto flash crash 15-25%, and continued their slide throughout the remainder of the week. Week-over-week, crypto prices fell north of 20%.

We study these markets all day, every day. We challenge assumptions internally, and externally, as best we can. And we try to be pragmatic when it comes to separating the real growth and maturation of this market versus the noise, manipulation and unrealistic expectations. But I honestly can’t remember a time when crypto price moves have made less sense.

No one has perfect clarity ahead of big moves, and fast and violent price action is obviously unpredictable, but it has historically been possible to at least rationalize a large move after the fact. Yet five days after this massive decline, there still haven’t been any valid explanations. The best explanation is that a rumor about hash rate declines (which has since been completely debunked) followed by a slow and disappointing launch for Bakkt’s new futures platform (any expectations other than a slow start were completely unrealistic) triggered the selling. This was then exacerbated further by a cascade of levered unwinds and massive stop loss liquidations. After that, market sentiment changed, and more importantly, a lack of cash on the sidelines became evident.

We’ve been discussing the levered unwind since June; a month where prices fell 15% in the first 10 days, rose 80% over the next 2 weeks, and subsequently fell 25% in the final week. In a market dominated by trading, monitoring leverage in the system is very important and often serves as a leading indicator to health and volatility. This leverage had been unwinding over the past three months, and even though leverage began to tick up over the past few weeks, that leverage was fairly equally distributed between longs and shorts. Given that backdrop, it’s perhaps even more surprising that short covering didn’t stem this decline quicker, especially since most market participants who were short were initially targeting re-entry long positions at levels only 5-10% lower. As we stand now, the continued selling pressure may be based on confusion, or fear, as the market tries to again regain equilibrium even though neither buyers nor sellers really understand why we’re here in the first place.

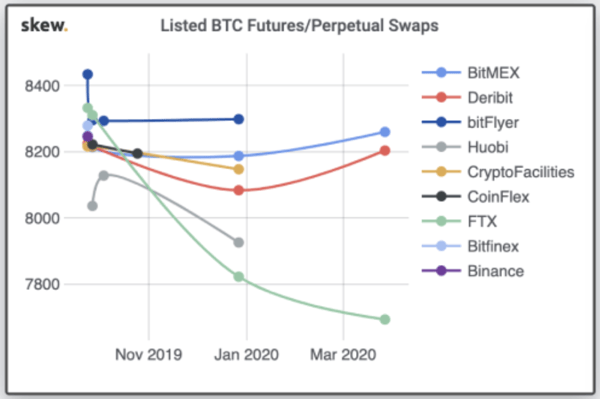

Further, the lack of “traditional pipes” in this financial ecosystem became evident once again. Part of the reason stop losses are hit so quickly is because there are no prime brokers, so each investor/trader has to post collateral individually at each trading venue and exchange, and that collateral is often not very deep. Moreover, the inability to quickly move cash and crypto assets freely and quickly resulted in very large dislocations. At one point on Tuesday, Bitcoin (BTC) was trading at a $500 premium to the price seen on other exchanges, especially those that offered leverage via futures and options (like Kraken, Bitmex, Binance and Deribit). As liquidations occured, via selling spot and forced futures selling, these imbalances grew. In a normal world with prime brokerage, arbitrageurs would quickly sell spot and buy futures and that arb would go away quickly, but in crypto, few were able to send BTC over to Coinbase fast enough to sell, and even fewer had enough collateral to buy futures at other exchanges. There were also market makers that were clearly caught offsides, which created arbs in the futures prices themselves as these market makers were forced sellers to get back onsides. These arbs and inefficiencies exist far longer than they should, and lead to even more panicked trading, all because of the inability to move digital assets around.

Dislocation of Futures Prices by Exchange on Tuesday, September 24th

Whatever the reason for this past week’s move, the results are another stark reminder that the crypto markets just aren’t quite ready for prime time. You can of course still invest in this space (and you should). And none of these problems invalidate all of the progress that has been made over the past year. But the best and biggest firms in this space are large trading shops, not large asset managers or retail crypto owners. And that means we’re still at the mercy of massive, liquidating swings. This will change over time. Most new asset classes are initially dominated by traders and market makers, but eventually, the long-only money grows to be the largest and most impactful. And in an asset class as small as crypto, inflows will assuredly be far greater than outflows over the next few years and decades.

Lost in the Declines are the Improving Fundamentals

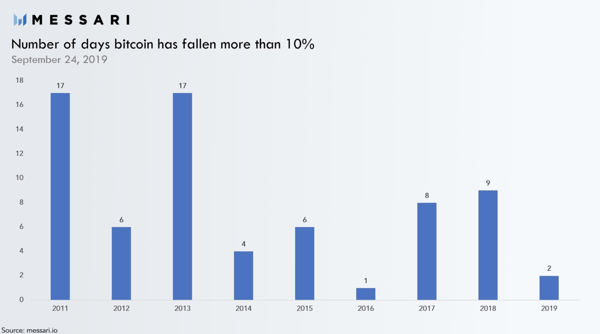

Lost in last week’s crypto declines is that the industry has never felt stronger. We highlighted the growth of Ethereum last week, and this week we’ll take a look at Bitcoin’s recent fundamentals. Not only should Bitcoin be benefiting from a perfect storm of macro factors (negative interest rates, more rate cuts, currency devaluations, recent banking stress as seen in the repo markets, etc), but at its core, Bitcoin is being used more than ever. Everything from hash rate to transaction volumes to number of wallets is growing, and we’re now only 8 months away from the “halving” event where Bitcoin’s inflation/supply schedule is set to cut in half. As long as demand remains constant, this will have an effect on price.

The fact that new buyers haven’t yet stepped in at these lower levels may be more indicative of a lack of cash in the ecosystem than truly negative sentiment. Which is ironic, because at the same time, cash outside of crypto is piling up faster than ever.

Expect this gap to close over the next 9-12 months.

Notable Movers and Shakers

The entire market moved in lockstep with Bitcoin’s massive price decline last week, leading to a week of poor performance across the board. A handful of assets did have significant news that should be reviewed:

- Amid the market decline last Tuesday, Binance US officially opened for business. Although the exchange has been accepting new accounts and deposits for a few weeks, trading officially began for the fiat-to-crypto platform. To start, customers are offered feeless trading until the beginning of November. Regardless, BNB ended the week down almost 19%.

- Last week Coinbase announced that its New York customers would have access to ChainLink (-7.66%), Algorand (-24.52%) and Stellar (9.71%). These assets were previously listed on Coinbase’s exchange earlier this year. New York state has much higher regulatory standards which likely led to the delay.

- Ripple announced last week that it acquired Logos through its investment arm Xpring. Logos is a startup focused on creating speed and scalability solutions in the payments space and the team will focus on building DeFi initiatives at Ripple. The terms of the acquisition have not been made public but this is the third Xpring deal this year.

What We’re Reading this Week

The implications of Quantitative Easing (QE) and Quantitative Tightening (QT) policies since the 2008 financial crisis are starting to come into stark relief in recent months, culminating with the repo rate spike. Such policies have led many to question the economy’s fate and how long individuals will stand by and accept money that is being inflated. Crypto however, will thrive in such an environment as a deflating asset. In addition, crypto does not only serve as a safe haven asset (similar to gold and silver), but also offers the freedom to move and flow easily, untethered to the banking system.

Understanding Negative Rates and How They Impact Crypto

Digital Asset Research inspects the difference between nominal and real negative rates to understand their impact on cryptocurrency. Real rates, which reflect interest rates minus inflation, are a better way to measure purchasing power versus nominal rates, which includes an inflation premium. Real rates, as seen on Treasury Inflation-Indexed Securities (TIPS), indicates that to keep apace with inflation, cash balances should be invested in non-risky assets. The move out of cash to other assets will therefore have the largest impact on non-productive assets such as Bitcoin.

Last week, the US House of Representatives passed a bill requiring FinCen to study the uses and implementation of various technologies including blockchain and AI. The goal is to understand how the department can leverage these technologies for data analysis and communication of data to various branches of government. Blockchain advocates are optimistic as the government embraces blockchain technology to “revolutionize entire sectors of the global economy”.

Social Finance (SoFi), a startup that assists with refinancing student loans, announced last week that it would begin offering cryptocurrency trading to its customers. According to SoFi’s CEO, crypto investing has been “the most requested service” from existing customers and will fit nicely alongside its app-based investing options which includes ETFs. SoFi plans to initially add support for BTC, ETH and LTC and will source the cryptocurrency through Coinbase. They are the latest in a string of fintech businesses to add support for crypto trading as consumer demand grows for these products.

According to Bloomberg, Venezuela’s central bank has begun exploring whether it can hold cryptocurrencies, at the request of the state-run oil producer, Petroleos de Venezuela SA (PDVSA). In recent years, PDVSA has found it difficult to accept payment from suppliers as international sanctions have made banks and other financial institutions wary of doing business with the oil supplier. Many are hypothesizing that PDVSA was therefore paid in crypto by its suppliers. They now face the challenge of figuring out how to change the crypto into cash and have turned to the central bank for assistance.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)

Source: Messari

Source: Messari