What happened this week in the Crypto markets?

More Anything? More Everything!

In a classic Seinfeld episode, Jerry was in the first class cabin and the flight attendant asked, “More anything?”, to which Jerry smugly replied, “More everything!”. Global Central Banks and governments are now granting this wish.

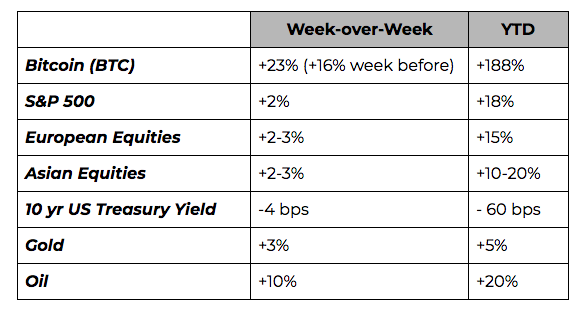

Week-over-week and YTD returns for global asset classes are nothing short of shocking. These are the types of markets that investors publicly celebrate, while secretly fearing.

Let’s start with non-crypto markets. Global equities fully embraced the more accommodative stance from the Fed, propelling the S&P 500 Index to its fifth all-time high of 2019 and marking the third straight week of gains (following a four-week losing streak during May). Oil jumped 10% on the heels of US-Iran tensions, as energy markets are slowly becoming as volatile as crypto (per data from General Risk Advisors: 6-month volatility for oil is now 1.74% and Nat Gas is 2.55%, vs Bitcoin at 3.26%and Global equities at 0.62%). US Treasuries meanwhile rallied to 3 year highs, with the 10yr US Treasury yield once again approaching 2.00%.

Unlike the crypto markets, there are multiple decades worth of data to suggest that mid-cycle rate cuts are a net negative for global equity markets, and that a recession is likely imminent. Between David Rosenberg’s frequent reminders about stretched equity valuations, to Jesse Columbo’s rants on the dangerous effects of global debt bubbles, to Raoul Pal’s data on rate cuts, there are certainly enough arguments to suggest that “don’t fight the Fed” may be getting a little long in the tooth. Cantor Fitzgerald may have put it best:

“Let’s just be frank: equity markets have become manic, hanging on every word from POTUS or Chairman Powell. Chairman Powell’s communication should have been no surprise, but it is somewhat disheartening that the Fed has come to consider itself as the guardian of infinite expansion rather than as an entity designed to smooth the natural course of business cycles. Without business cycles, capitalism loses its identity. We expect the Pavlovian response for global equities to be a rally on any dovishness as investors continue to lack context about what this dovishness really means. Perhaps, real economies don’t really matter anymore and the eventual move towards central bank ownership of all assets by the time our children are middle-aged gives market participants comfort. Moreover, a concept from Economics 101 seems to have been forgotten by bankers and investors alike: diminishing marginal benefits (not to mention unintended consequences). Central bankers have become a bit like a adolescents succumbing to peer pressure– daring each other at every turn - to implement the policies about which many wrote their PhD theses.”

There is a reason that equity and fixed income Hedge Fund managers have almost universally underperformed passive investment strategies for the past 10 years -- during broad-based rallies where bad news is good news, the risks accelerate, leading to more downside protection. But long-only, 100% invested indexes don't care about growing risks.

Facebook Was the Final Catalyst, But This Crypto Rally is a Bit Unsettling

Meanwhile, the crypto markets were on fire for the second straight week, blowing past all resistance levels and gaining an additional 15% since Thursday alone. Over the past 5 months, Bitcoin has gained 12% (February), 8% (March), 29% (April), 62% (May) and 24% (June MTD).

On the heels of Bitcoin’s historic rise, there is no doubt you heard about digital assets last week, especially after Facebook officially released its whitepaper for a new digital payments system. This dominated the news, and stretched far beyond typical crypto news coverage. We were even asked to join Fox Business and Yahoo Finance last week, where of course we were forced to answer questions about Facebook’s new coin (we wrote last week that Facebook is the tipping point for crypto).

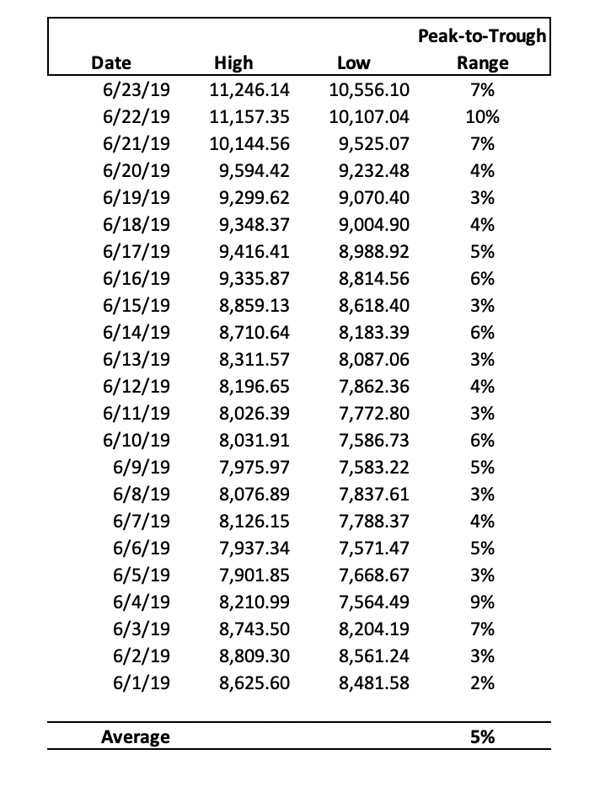

We too are excited for the long-term potential of digital assets, including Bitcoin. But in general, when global markets go parabolic, it's often wise to exercise a hint of caution in the near-term. Bitcoin has now averaged 6% intraday swings for the entire month of June, which would make any disciplined and responsible investor take pause, and probably reduce position sizes, even if the trend continues higher.

Bitcoin Price Chart & Intra-day Volatility

Source: CoinMarketCap & Arca Proprietary

What is perhaps most interesting in crypto is that many of the positive factors that we've been talking about for months, which certainly helped propel the market’s advances YTD, are now sitting plainly in the rear-view mirror.

- Bakkt, Fidelity, and Facebook have now all officially set launch dates, and FB’s actual product is still 1 year away

- The Yuan has stopped depreciating towards the critical 7.00 level, and is now strengthening

- The trade wars are potentially coming to an end

This of course does not mean crypto rally price increases need to, or should, stop -- but it definitely makes us wonder what will be the next real catalyst for adoption. And the longer term picture for digital assets is of course still as strong as ever. Mike Creadon at Drawbridge Lending pointed out some startling numbers over the weekend: There is more than 65 times more money in the world invested in negative-yield bonds ($13 trillion) than there is in bitcoin ($200 billion). Every global Central Bank action that reduces purchasing power, adds debt, and increases systemic risk, is a net positive for Bitcoin and every other digital asset. Further, the asset-light economy (AirBNB, Uber, Google, etc) tells you all you need to know about whether or not younger generations will substitute hard assets with digital representations (they will).

But when it becomes a forgone conclusion that crypto markets are going higher, and every taxi driver and grandmother is talking about it, it becomes a bit unsettling. Earlier in the year, bullish sentiment was offset by equal and constant skepticism, but we’re now entering a point of euphoria unseen since late 2017. Prices are skyrocketing on low-volume, weekend algos gone wild.

A Look into the Fundamentals and Technicals

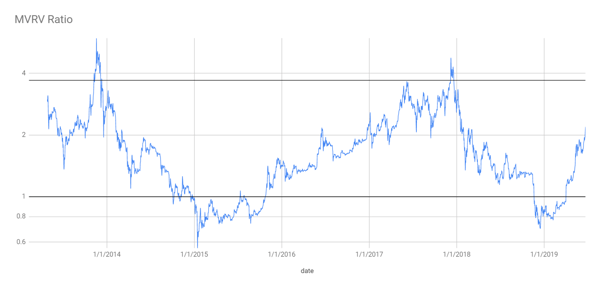

This space is still evolving, but there have been a lot of advancements in crypto valuation techniques over the past few years. While some “security-like” digital assets can be modeled using traditional DCF-like tools, other more traditional “money-like” cryptocurrencies (like Bitcoin) require more of a supply/demand type of analysis. Currently, many of these indicators are flashing overbought signals.

For example, the popular MVRV ratio is increasing at a much steeper slope than during previous bull runs. There haven’t been any pullbacks in the MVRV ratio, which is uncharacteristic compared to the last bull run. Though not yet above the overvalued zone of 3.7, the slope of MVRV is similar to that of late Bitcoin market cycles.

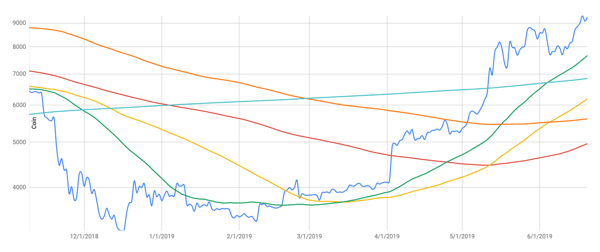

From a technical perspective, when Bitcoin first hit 10,000, Bitcoin continuously pulled back to the moving average. Compared to the most recent break of Bitcoin $10,000, throughout this advance we have not touched or pulled back to any significant Moving Average.

We’ll be watching metrics like these, and others, very closely over the next few weeks. That said, our near-term hesitation does not at all take away from our long-term bullishness. Those who can withstand high levels of volatility should rightfully ignore any near-term hiccups. Those in the “protection of capital” business should probably heed these warnings.

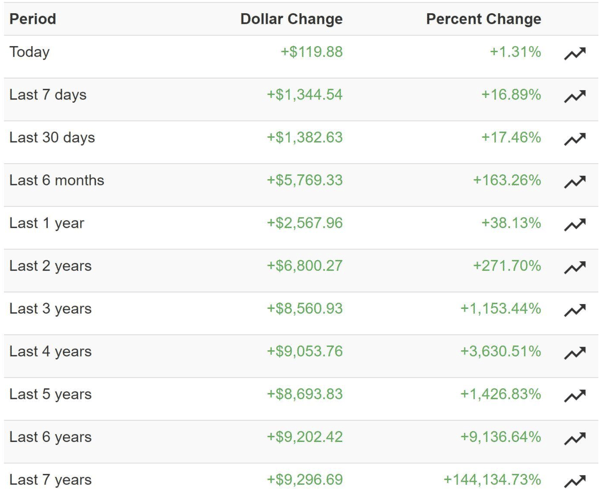

Over Longer Time Horizons, Bitcoin has Been Hard to Beat

Notable Movers and Shakers

Bitcoin continued to capture market share last week, finishing up 23% (with Dominance up to 59.2%). The last time Bitcoin Dominance was this high, Bitcoin was again at $11,000 USD (December 4th, 2017). With Bitcoin dominating headlines in the digital asset space this week, it was easy to miss some developments out of the alt coins. Nonetheless, there were some projects that stood out:

- Ripple (XRP) announced Monday that they partnered with MoneyGram, a money transfer service that will push out the xRapid cross-border payment system that utilizes XRP. This news in of itself did not have a significant impact on XRP price (+7.5%), but it is worth noting that MoneyGram stock went up as much as 169% after hours, which can be attributed to Ripple acquiring an 8-10% stake in the company at $4.10 a share (when announced, MGI was trading at $1.44).

- Algorand (ALGO) has been the talk of the town for a few weeks now, but finally listed on Thursday after a successful Dutch Auction ($2.40), raising $60M (implied $6B market cap). This particular raise was significant, as Algorand offered a 1 year put option at 90% of the auction clearing price ($2.16). With Algorand planning to auction off 600M ALGO per year for 5 years, it seems as if this token will be at the forefront of financial conversations in the digital assets space for years to come. That being said, ALGO finished the week down 49% ($1.66), a significant delta from the put option that matures in a little under a year.

- Neo (NEO) finished the week strong (+25%) - their decentralized exchange NASH is set to launch its beta soon. Neo (formerly AntShares) was a market darling in 2017, receiving massive hype as the “Ethereum of China” - since then, it hasn’t made much noise. NASH might be their first attempt to re-enter the crypto mainstage.

What We’re Reading this Week

Libra is all anyone could talk about last week, as both crypto news and mainstream media fawned over it (it was even featured on Comedy Central’s “The Daily Show”). One thing to pay attention to are the regulatory hurdles that Libra and Facebook will have to overcome in order to become a global currency as promised in their white paper. After announcing their ambitions last week, members of the US Congress called for the project to halt until it could be examined more closely. The Senate Banking Committee now has a hearing scheduled with Facebook next month to examine the project and “data privacy considerations”.

Grayscale Investments, the firm that offers the Bitcoin Trust (GBTC), provides an in depth review of what happens to Bitcoin in times of crisis. With global debt at an all-time high ($250T), Bitcoin offers an attractive method to hedge the risk of currency devaluation. Specifically, they touch on five past macroeconomic developments and Bitcoin’s subsequent price action to support this thesis: Grexit (2015), Economic Concerns in China (2015-16), Brexit (2016), Rising Geopolitical Risk & Tighter US Financial Conditions (2016), and US China Trade Tensions (2019).

Insurance carrier MetLife announced last week that it would be creating an Ethereum-based pilot platform for life insurance claims. The platform, dubbed “Lifechain” would add transparency and efficiency to a difficult process for most individuals filing insurance claims after the loss of a loved one. The program will use the number issued on death certificates to verify if the deceased had a life insurance policy and begin the claims process without the paperwork hassle for family members. Although this is promising for public blockchains, the program will only be available to 1,000 users in Singapore.

Oil and natural gas producers have a common problem: natural gas venting, which occurs when natural gas seeps out of a pipe into the atmosphere, is wasteful and produces additional Green House Gas (GHG) emissions. Producers have not had an effective way of capturing this gas and monetizing it until now. Bitcoin mining, which requires low cost energy, can use the excess natural gas to power mining data centers, eliminating the excess GHG and monetizing the lost natural gas for oil producers. Upstream Data began creating portable mining centers in 2017 for this purpose - disproving the “Bitcoin is bad for the environment” narrative.

QuadrigaCX, the Canadian crypto exchange that lost over $200m in customer funds late last year, was back in the news last week after a new report from Ernst & Young revealed the deceased CEO mismanaged customer funds. The report details how Gerald Cotton ran most of the business from his laptop and transferred out customer funds to rival exchanges between 2016 and 2019. On these outside exchanges, Cotton traded digital assets in his personal name and had “substantial losses”. The conclusion: the firm had very few operational or financial controls in place to protect its customers.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)