What happened this week in the Crypto markets?

Honestly, Not a Lot -- and That’s Great!

The crypto markets gained roughly 3% during a pretty uneventful week, with most of the gains coming during a short burst higher on Friday. There were, of course, a fair amount of high-flying small-cap tokens that gained north of 20%, many of which are unheard of, as well as the typical retracements of a few high flyers from previous weeks that ran too far, too fast and fell over 10% week-over-week. But overall, it was a listless week for crypto.

But boring isn’t a bad thing.

But boring isn’t a bad thing.

This is often lost on traders who prefer volatility. And the crypto markets are unfortunately mostly made up of traders and other individuals who think they are traders. But boring can actually be a good thing. Just ask fixed income fund managers and any other income-producing fund managers.

I’m reminded of 2016 and early 2017 when equities rallied every day and the high yield bond market was trading at all-time low yields and tight spreads, amidst record low default rates. I recall calling a friend of mine who traded for a $20 billion credit hedge fund, and the conversation went something like this:

Me: “How are the markets treating you?”

Trader: “Painful. It’s so boring.”

Me: “Sorry to hear that.”

Trader: “Don’t be -- it’s great for business. We’re clipping a coupon and our investors are happy.”

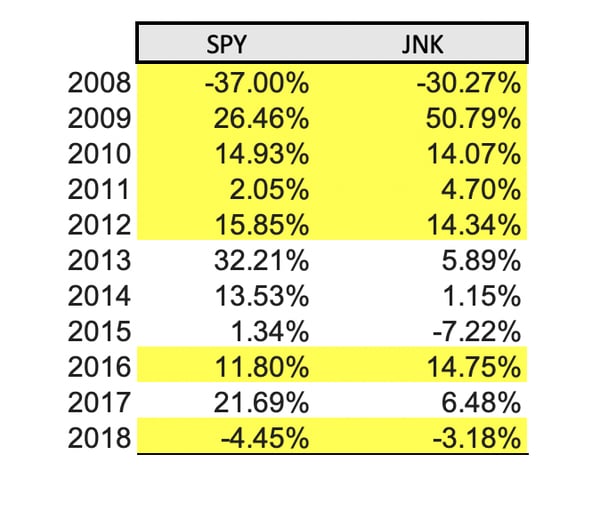

The High Yield bond market is unique. It’s one of the few asset classes that creates both high income and high beta. As a result, the High Yield market can outperform all other asset classes in both down years and up years, and performs especially well when market conditions are relatively stable.

High Yield Bonds (JNK) Can Outperform Equities (SPY) In Both Up & Down Years

The crypto markets are starting to behave similarly. With the advent of Decentralized Finance (think banking services without the bank), there is a marketplace blossoming that includes lending, borrowing, mining and staking services which allows owners of digital assets to earn a yield on their holdings. Sure, when crypto markets are volatile you can make a lot of money. But when crypto markets are stable and volatility decreases, you can earn yields of 6-10% by lending your tokens or by selling covered calls or volatility via the up and coming derivatives market. These rates look especially attractive given the current shape of the Treasury yield curve. And unlike High Yield bonds, which actually have negative asymmetry since the potential downside is much larger than the capped upside, crypto still offers the most positive asymmetry of any asset class available today.

The crypto markets are starting to behave similarly. With the advent of Decentralized Finance (think banking services without the bank), there is a marketplace blossoming that includes lending, borrowing, mining and staking services which allows owners of digital assets to earn a yield on their holdings. Sure, when crypto markets are volatile you can make a lot of money. But when crypto markets are stable and volatility decreases, you can earn yields of 6-10% by lending your tokens or by selling covered calls or volatility via the up and coming derivatives market. These rates look especially attractive given the current shape of the Treasury yield curve. And unlike High Yield bonds, which actually have negative asymmetry since the potential downside is much larger than the capped upside, crypto still offers the most positive asymmetry of any asset class available today. It’s the best of both worlds -- high income and unlimited upside potential.

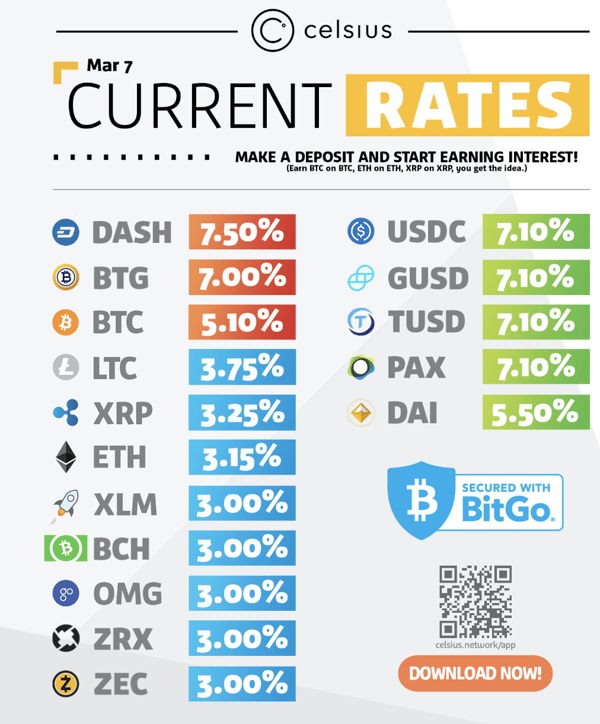

Sample Rates Earned By Lending Long Crypto Positions

There are a lot of reasons why some investors are still on the sidelines when it comes to crypto. But it’s worthwhile to remember what problems crypto actually solves for in the first place. A mistrust of centralized banks, a lack of investable assets, and most importantly, the removal of hundreds of unnecessary middlemen that result in exorbitant fees.

LendingTree’s slogan for mortgages is “When Banks compete, you win”. But when banks become unnecessary, we all win more.

A Noteworthy Trend

I visited the AltsLA conference last week, which hosted a wide representation of Alternative fund managers, institutional investors and service providers. As expected, the heavyweights were there… Blackrock, Citgo, Aberdeen, EisnerAmper, Harvest Exchange and hundreds of others, with only a small but important subset focused exclusively on crypto and blockchain.

But one booth, in particular, caught my eye. Fidelity wasn’t there, but Fidelity Digital Assets was. It was a pretty strong statement that Fidelity sent it’s “B team” to a well-attended alts conference where only a handful of attendees could be pre-identified as crypto enthusiasts. And as you can imagine, their booth was crowded… very crowded. Trust matters, and Fidelity has earned it for over 75 years. If you don’t think this moves the needle, you’re watching the wrong needle.

Notable Movers and Shakers

- Small-caps continue to outperform, with most of the strength coming from the gaming sector (WAX, ENJ, LOOM). The newest trend last week was the strength of this year's laggards -- many tokens that hadn’t rallied at all this year (like BCH, GO, OMG, XLM) were all up 10%, which is likely due to relative value as investors are rotating out of the winners and into the losers.

- Stellar (XLM) gained 10% after Coinbase listed the token on its platform, and also following an update of their logo ahead of a planned announcement with IBM at Money 2020 Asia this week.

- KuCoin Shares (KCS) are up 54% on the back of BNB’s success over the past several weeks, a piggybacking trend we are now seeing across several sectors. The exchange rewards KCS holders dividends worth 50% of all trading fees generated by the platform.

- Blockchain application platform, Lisk (LISK), rose 20% after announcing a partnership with WEG Bank, along with Litecoin (LTC) and TokenPay (TPAY) - the latter is up 54%. The original partnership between TokenPay, Litecoin and WEG Bank was announced last November.

- Cosmos’ long anticipated mainnet launched early last week, with its token ATOM, beginning trading on Thursday. Cosmos, which raised a $17m ICO back in 2017, is an interoperability solution that aims to connect all different blockchains seamlessly.

- Decred (DCR), a self-governed, decentralized currency, gained 16% last week following its listing on the OKCoin exchange. Although we’ve seen exchange listings offer less and less price appreciation (see above regarding Stellar), occasionally it can have a positive impact, for example when offering fiat trading pairs.

What We’re Reading this Week

Collateralized Fund Obligations, bond funds backed by stakes in hedge funds and private equity funds, are the new financial Frankenstein, according to this Bloomberg op-ed. If this sounds familiar, the idea is similar to Collateralized Debt and Loan Obligations, which helped cause the financial crisis of 2008. This is the type of financial engineering you see at the top of the cycle when investors are searching for yield and differentiated returns. Naturally, we ask ourselves “Are there not better alternatives to earn differentiated returns (i.e. crypto)?

Hedge fund billionaire Alan Howard’s Elwood Asset Management is planning to launch a range of institutional products for the digital asset space. The first product, a blockchain ETF launched with the help of Invesco, will “target companies with the potential to generate real earnings from blockchain technology”.

Legendary VC investor, Fred Wilson, shared his thoughts on Decentralized Financial (DeFi) and why its growth is so important to blockchain/crypto right now. He argues that unlike all the other use cases that demand scalability (gaming, media, e-commerce), DeFi is managing to catch on and offer real use cases for crypto beyond trading and speculation.

Tether, the first stable token on the market, was back in the news again last week after they quietly updated their terms, stating that their reserves may not in fact actually be 100% backed by USD. We wrote about Tether last year when questions first arose about its supposed 1:1 reserves, as each Tether issued is supposedly backed by $1 USD. The impact on the crypto market this time around was muted, but these skeletons in the closet add systemic risk.

In this presentation from venture firm, Kleiner Perkins, the firm recounts the state of crypto, major accomplishments of 2018 and their five focus areas heading into the next year. Despite the crypto winter, Kleiner is still bulled up on the space and watching for the next wave of innovation.

Last week, famed investor Marc Faber, who famously predicted the 1987 stock market crash, revealed that he bought some Bitcoin. As a skeptic of the digital asset a few years ago, Faber now claims that he bought it as the technicals “look better”.

Identity blockchain project Civic (CVC), debuted a beer vending machine at SXSW last week, which verifies a buyers age and accepts payment in crypto. Attendees were able to purchase beer using CVC tokens which were airdropped to them at the conference. The machine will set you back $15,000 or 1,372,363 CVC.

Arca in the Press & on the Streets

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA — Chief Investment Officer

Katie Talati — VP, Research

Hassan Bassiri, CFA — VP, Portfolio Management

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)