What happened this week in the Crypto markets?

A Long Road Ahead

Many have compared the events of this past week to September 2008. Others have drawn parallels to 9/11. Some have even compared this to 1918. Those events all had incredibly long-lasting impacts.

We’re just now entering week 6. We could be in for a long, bumpy ride ahead.

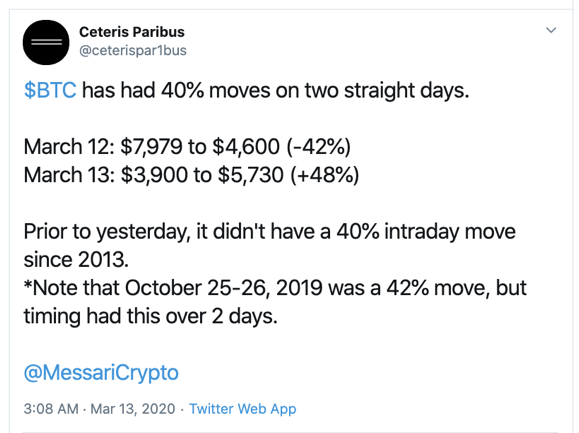

The final week-over-week numbers were of course dizzying...

- S&P 500: -9%

- Gold: -8%

- Oil: -33%

- Bitcoin: -34%

Source: CNBC, TradingView, CoinMarketcap

… but how we got there was even more gut-wrenching. US equities closed up or down by more than 4% every day last week, which was the first time that has happened since 1929. This included three daily moves of almost 10%, with Friday’s short-covering rally occurring almost entirely in the last 45 minutes of trading. Oil’s precipitous 30% drop happened in just 24 hours, and oil oscillated in 10% intraday swings thereafter. Bitcoin digital assets was down almost 50% on Thursday, with numerous 10-20% swings immediately after. Treasuries had virtually no bid at one point. There are also rumors of very large hedge funds imploding, prompting the initial $1.5 trillion repo expansion from the Fed.

The path has been violent to say the least, and this of course has led to more of the same responses from governments around the world. The Fed has stepped in with rate cuts and QE, while other countries have gone further with both monetary and fiscal stimulus (Germany to suspend constitutional debt limits temporarily, Hong Kong to give HK$10,000 in cash to residents, Italy suspends tax payments, South Korea bans short selling). The coordinated global response over the weekend was reminiscent of 2011. The irony of hoping to be saved by the same people who pushed you off the bridge is troublesome.

But despite negativity everywhere, it is almost certain that it won’t be a straight line down from here.

Most people recall when JP Morgan bailed out Bear Stearns in March 2008 for $2/share (from a high of $171/share in 2007), but some have forgotten that the problems first surfaced in a rather innocuous way back in June 2007.

At the time, the problems were deemed to be caused by a few rogue traders, and it was assumed that they were completely isolated (similar to the world’s initial response to COVID-19). In retrospect, we now know that the problems at the two Bear Stearns hedge funds were not at all contained at Bear Stearns and foreshadowed the entire mortgage crisis that culminated 12 months later. Further, not only did it take another 9 months for Bear Stearns to ultimately collapse, but the S&P 500 actually traded UP from July 2007 to October 2007 following the initial Bear Stearns news, reaching an 8-year high in October 2007, and then traded up again from March 2008 to June 2008 following the complete collapse of Bear Stearns. Of course, the market ultimately fell 50% from the highs through the March 2009 lows.

Drawing parallels to today, perhaps:

- September 2019 Repo Market implosion = June 2007 Bear Stearns hedge fund collapse

- COVID-19 & Oil war = March 2008 Bear Stearns bankruptcy

- ???? = September 2008 Lehman / AIG collapse

Maybe we’re heading towards a major healthcare breakdown, massive corporate bankruptcies, modern monetary theory, or something entirely different. But there is a good chance markets rally much further than people expect just like they have fallen much further than many expected. While the immediate reaction to this week’s government stimulus actions were negative, any progress demonstrated in containing the spread of COVID-19 may give markets a jolt, even if bankruptcies and a major recession are still on the horizon. To state the obvious, no one knows.

The Crypto Market Structurally Broke

While global markets broke down last week, crypto markets may have structurally broken. Decentralized finance (DeFi) nearly collapsed as the price of Ethereum (ETH) fell 60% (ETH is used as collateral and serves as the backbone and pipes for much of DeFi). Meanwhile, top crypto exchanges buckled, and temporarily shut down under the weight of liquidations and stop losses.

Thursday was one of the worst days on record for Bitcoin prices and other digital assets, yet it was also one of the fastest recoveries. The crypto market ALMOST died, but it did not die.

That said, while we don’t trivialize the losses in crypto, there was something kind of beautiful about the community-based losses felt by the crypto investment world versus the constant intervention needed to make traditional markets function. This past week, circuit breakers shut down the equity markets multiple times, short selling bans were enacted, repo markets were artificially propped up, interest rates were manipulated, and the only legal cartel in the world (OPEC) interfered. Trillions of dollars in capital injections occurred, with more to come, just to stabilize a market that is still close to all-time highs. The paper gains made from Friday’s equity rally alone ($2-3 Trillion) dwarf the entire size of the digital assets industry (sub-$200 billion).

So yes, digital asset prices were cut in half, but the crypto market did not require artificial intervention to survive and continue working. It is, by definition, antifragile. The industry is feeling serious pain right now. Many are suffering. But the industry is already rebuilding and fixing mistakes. The concept of “Creative Destruction”, coined by Austrian economist Joseph Schumpeter, describes the process of growth that comes from free markets that allow lost jobs, ruined companies and vanishing industries to occur. Those that stick around for the growth will likely be heavily rewarded.

Forest fires are analogous. When forests are allowed to burn, the weak sections die off and the forest grows back stronger and more prepared to withstand the next natural disaster. But if you keep sending the fire department every time there is a tiny brush fire, the forest never burns down and therefore can’t rebuild strong enough to combat the next large fire. We may be seeing that now in equity and credit markets.

Meanwhile the crypto markets break all the time, and each time they have come back stronger. The losses are real. Measuring VAR and sharpe ratio is exhausting amidst this volatility. But the end product may be better than anything currently available. Projects that have no reason to exist will likely die; while those with real utility and/or real value capture ultimately will recover. It is refreshing, albeit nearly impossible to navigate. And at the end of the day, what you own in digital assets is yours to use and spend. Should this global decentralized experiment ultimately succeed, the losses in dollar terms ultimately won’t matter.

Digital assets are certainly not going away. The distressed buying environment was simply accelerated by free markets.

What About the Safe Haven Narrative?

Frequent readers of “That’s Our Two Satoshis” know that we’ve tried to be pragmatic when it comes to crypto market narratives, while also pointing out the hypocrisy of other asset classes that are also built on narratives. But there is little doubt that the “Bitcoin is a safe haven” narrative took a severe blow last week. Many owners of Bitcoin predicted this exact scenario, and yet are still losing money. Similarly, Ray Dalio has nailed the macro call, yet is facing massive losses. As always, identifying the thesis is the easy part, but finding the correct way to express that thesis is difficult, especially when results are measured by the minute.

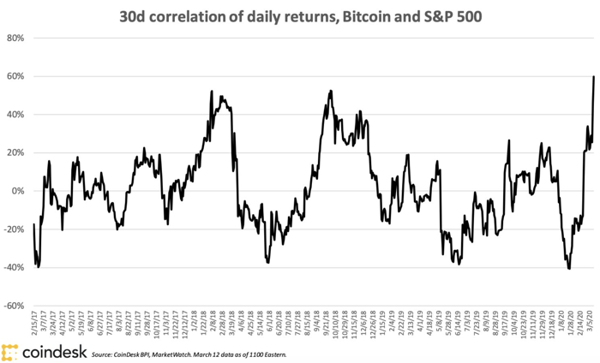

The typical non-correlated nature of crypto has quickly become almost fully correlated to equities. Not only is this unsettling for those looking for Bitcoin to hedge their portfolios in real-time (though we’ve argued against that numerous times), but it has also turned a bunch of inexperienced young crypto developers into stock watchers.

While correlations have clearly risen, it’s still difficult to determine how much the outside world really impacts crypto prices. Clearly the “risk-off” mentality caused the selling wave in crypto (kicked off by the decline in oil last week), and now the “crypto follows stocks” narrative is in play temporarily. But digital assets are physically held in different locations than other risk assets. In fact, other than on the CME, there is almost no overlap between digital assets and traditional asset classes. As such, there really is no impetus for cross-asset selling like there is in gold, bond and stock markets. Every dollar raised via selling ultimately sits in the crypto ecosystem, ready to be redeployed at some point with nowhere else to spend it.

Given historical correlations are virtually non-existent, it’s likely that this pattern will end soon, perhaps as early as this week as market participants begin to absorb what all of this government stimulus really means. It is, of course, somewhat ironic that in an industry built upon lack of trust in governments, the knee-jerk reaction is to sit in US dollars.

“How will we pay for it?”

With government stimulus printing presses working full stop, "How will we pay for it?" began trending on Twitter over the last few days, indicating both a moral hazard (everyone expecting massive stimulus), a sign of frustration (income inequality, more bank bailouts), and growing political unrest during an election year.

Recall, the bank bailouts from 2009 sparked the genesis of Bitcoin -- 10 years later, the need for less government, more decentralization, and less "too big to fail" companies still resides. Worth noting that this article, suggesting a tax cut so Americans could buy more stocks, came out on Feb 14th, before any of the events of the last 3 weeks even unfolded. So while the “Bitcoin is a safe-haven” narrative may have died from a trader’s perspective, from a purchasing power perspective and as a shield from systemic risks caused by governments and banks, nothing has really changed. Fiat currencies will lose value -- and those who chose to protect against that risk in ways other than inflation protected assets will likely continue to flock to Bitcoin and other digital assets that create value beyond revenues and profits.

The biggest impediment to digital asset adoption has always been convincing investors to own more than just equities. Our biggest competitor was complacency and status quo. Well, the first part of that conversation is no longer required. The second part will be based on how this nascent asset class responds once the fear and panic subside. In our view, the world needs Digital Assets to work now more than ever.

What We’re Reading this Week

Much of last week’s market news was focused on Bitcoin and the broader market decline, but many missed what the decline meant for Ethereum’s decentralized finance (DeFi) ecosystem. Last Thursday, as many rushed to use the Ethereum network during the market’s meltdown, many DeFi applications malfunctioned or ceased to work completely. Specifically, “oracles”, which feed prices from the outside world into these applications, and smart contracts were unable to keep up with the violent market moves leading to delayed price readings into DeFi. The events of Thursday shed light on the shortcomings of DeFi and have outlined the improvements that need to be made before mainstream adoption can be reached.

Morningstar has for the first time issued a rating on a blockchain-based security. The issuer is FAT Brands, the owner of Fatburger, Buffalo Wild Wings and other fast casual restaurants. The debt financing is backed by franchise fees, royalties and upfront fees from its restaurants and was partially issued on Ethereum in the form of ERC-20 tokens. Morningstar cites speed and increased transparency as the benefits of using Ethereum for securities issuance. We expect to see many similar offerings issued via Ethereum and other platforms as companies look to take advantage of blockchain technology.

GoTrade Direct, a platform designed by aerospace giant Honeywell, is now tracking $1 billion worth of Boeing parts. The blockchain-based platform is designed to track the origin of parts and ensure they comply with safety standards. Boeing added the excess airplane parts early last week that were no longer needed. Currently, airplane parts are tracked using paper methods which are difficult to track and have the potential to be forged. The introduction of GoTrade Direct’s platform could potentially digitize an incredibly manual process.

In a recently published agenda for the negotiation of a Free Trade Agreement (FTA) with the United States, the UK identifies blockchain as one area that will benefit from the agreement. The newly proposed FTA, resulting from Brexit, proposes that the UK and US work together “in areas such as data flows, blockchain, driverless cars and quantum technology” to create the framework for global standards. Although no other specifics are given and there is no guarantee this will end up in the final agreement, the mention of blockchain signifies that the UK has the technology front of mind for the future.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)