What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

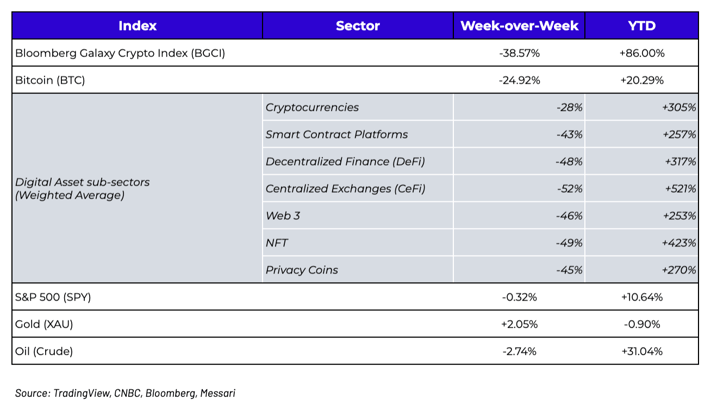

Week-over-Week Price Changes (as of Sunday, 5/16/21)

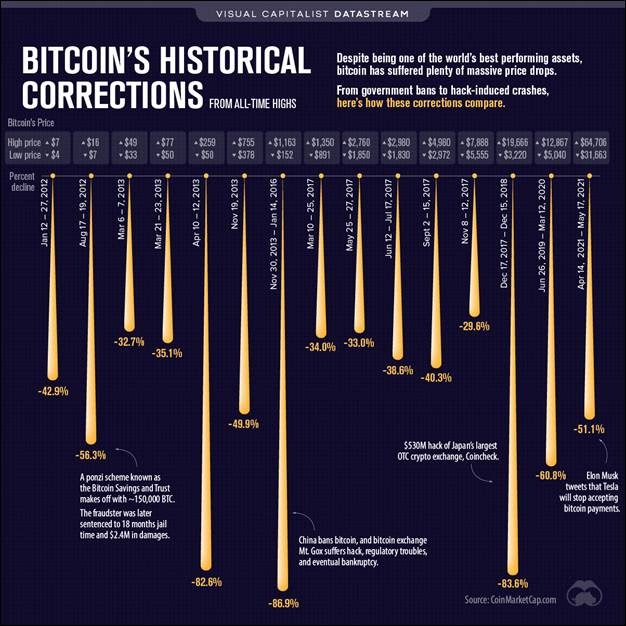

A Correction Like No Every Other

Last week was plain ugly. For newcomers, this was shocking. For old hats, this was perhaps nothing new, but unbelievably swift nonetheless. For perspective, using Bitcoin as a proxy for the market, let’s just say “we’ve been here before”.

Source: Cliffwater

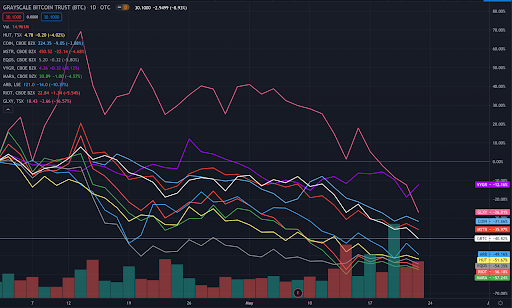

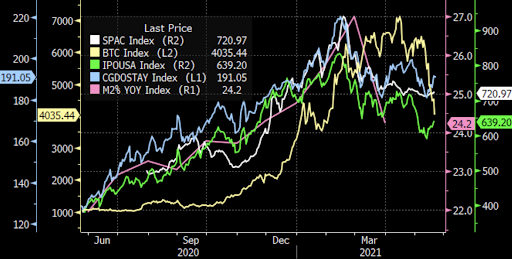

But there was something a bit more unsettling about the speed, and cause, of this pullback. We’re going to get to China and ESG in a minute, but let’s start by acknowledging that the broad-based moves across the digital assets market were due to a lot of factors beyond just China. First, we’ve seen a huge pullback in crypto stocks since mid-April.

Source: TradingView

Second, the inflation/tapering narrative is weighing on all risky assets -- tech stocks, IPOs, SPACs and digital assets all peaked around the same time that the U.S. M2 year-over-year growth rate peaked and rolled over.

Third, large Bitcoin put buying led to a gamma squeeze in the derivatives dealer community, which led to momentum traders piling on the short side and pushing the market over a cliff.

The above factors won’t get much press, but they all started long before Elon Musk tweeted about Bitcoin’s energy usage, and Friday’s subsequent news out of China.

The Largest Coordinated Attack in History

There are now hundreds of articles summarizing what the news out of China means, but at present, there is literally no definitive information other than the initial statement which came at 11pm local time on Friday night in China. Our friends at GSR and FTX summarized it well that day in their morning note to clients:

GSR: “Bitcoin fell sharply after a Chinese government website posted a statement earlier today summarizing the last meeting of the Financial Stability and Development Committee of the State Council. Chaired by Vice Premier Liu He, the Council’s statement singled out BTC as an asset it needs to regulate more. The statement said that China should crack down on BTC mining and trading and “resolutely prevent the transmission of individual risks to society”. This is noteworthy because Liu is the most senior Chinese official to publicly call for a crackdown on BTC. This is also the first time the government has explicitly targeted BTC mining. BTC mining is a big business in China and ~75% of the world’s BTC mining is done in China, where there is cheap electricity and relatively easy access to manufacturers who make specialized hardware. This crackdown on mining may be related to Musk’s recent comments about BTC’s energy consumption. The Chinese government made a commitment to carbon neutrality last year and reports of China cracking down on energy-intensive BTC mining operations have been trickling in over the past few weeks. BTC mining was banned in China’s Inner Mongolian province last month. This province is the country’s second-largest coal producer and earlier today the local government set up a dedicated whistleblower hotline to comprehensively shut down any illegal mining operations in the region. BTC mining operations in Sichuan have been operating at a limited capacity since the state has mandated them to limit their hydroelectricity consumption due to an unusually warm May.”

FTX: “The last leg lower on Friday was driven by China headlines on mining and trading. It's always difficult to interpret policy in China. It seems most likely that the comment is aimed at mining and focused on both the ESG and protecting capital flight (which is often facilitated by investments in BTC mining). This may have been as a verbal concession to the environmental lobby though mining uses a lot of renewable energy and also energy that wont be used otherwise. A larger crackdown on mining in China would actually lessen two areas of concern for crypto - centralized mining in China and removing some of the dirtier energy consumption.”

That said, make no mistake about it, the final leg of this downtrade was a global, coordinated attack on Bitcoin. Eric Peters, CIO of One River Asset Management, summed it up succinctly.

In human history, no single asset has come under such coordinated assault by the very global institutions that perpetually inflate asset prices in the name of securing prosperity. And yet, through it all, digital asset trading carried on, obliterating the leveraged longs, wiping out the weak. For the first time in decades, we saw the ferocious beauty of truly free markets operating at scale. Efficiently. Ruthlessly. These assets inhabit a world without a buyer of last resort to bail out its bankers. It was a remarkable display of antifragility. To appreciate it fully, simply imagine how today’s equity, bond and credit markets would withstand a withdrawal of government support, let alone a full-frontal assault. It is this independence and resiliency that underpins the longer-term attractiveness of digital assets. But like all powerful new technologies, their promise is poorly understood by most pundits. And amongst the many benefits that such technologies will produce, one of the more ironic is that despite today’s outcry, they have already begun to spur and finance an accelerating global transition to renewable energy.

In 2011, governments around the world conspired to rescue global markets from a double-dip recession. Now, they are conspiring to kill the only free market left which coincidentally rose from the ashes of that same government liquidity response. There is a bull case here though. First, long-term, removing China’s dominance over Bitcoin should lead to a reduction in Bitcoin’s carbon footprint and an increase in security. Second, the US regulatory crackdown is actually setting the stage for a sustainable policy, one where it’s pretty easy to comply with the laws as long as you aren’t purposefully trying to evade them.

Regardless, it is pretty amazing that in a year flanked by government overreach, massive monetary and fiscal stimulus, and inflation/taper talk, Bitcoin is only +20% YTD.

Perhaps even more interesting is that in a week dominated by Bitcoin-specific negative news, Bitcoin actually outperformed the rest of the digital assets market.

A Massive 4-day Selloff in Layer 1 Protocols, DeFi, CeFi and other Pass-Through Tokens

Just five days ago, Bitcoin was selling off while other digital assets were thriving, a response that was perfectly rational given all of the negative news directly aimed towards Bitcoin. But beginning Wednesday, accelerating Friday, and puking all over itself on Sunday, was the rest of the digital assets market. The speed of these declines was breathtaking. Correlations rose to 1.0, betas rose to 3-5x, and seemingly no asset was safe.

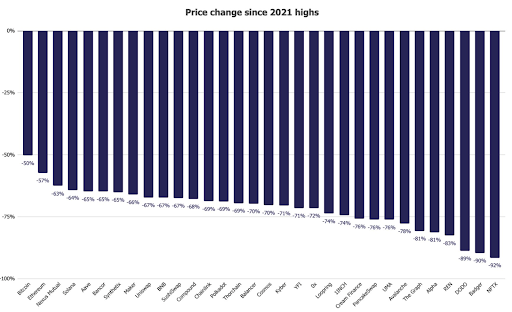

Declines from All-Time-Highs for Select, Popular Digital Assets

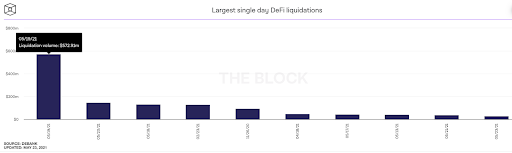

But DeFi Passed a Major Stress Test

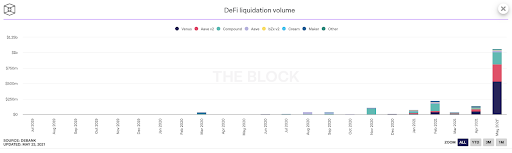

Throughout the carnage though, there were a few clear winners. First, DeFi passed a major stress test. There were over $10 billion of futures liquidations on Wednesday last week, and $1 billion more on Decentralized trading platforms and lending platforms.

But while their CeFi counterparts had technical issues, delayed fund transfers, and at times were down altogether, DeFi worked exactly as designed, handling all-time-high volumes and record liquidations without even a hiccup. As Camillo Russo of the Defiant put it, “As Ethereum DeFi grows to hold $100B in assets with millions of users, yesterday was a test on whether the space that aims to become the future of finance can withstand extreme volatility without breaking – and it passed.” Jim Bianco had a similar take, arguing, “... while most are focused on wild price swings and unusual coins, understand it was the traditional financial exchanges that failed investors again, not decentralized finance. Those arguing they are creating a new better financial system won the day.”

So Where Do We Go From Here?

Fundamentals will matter again. Maybe not right now, as the market is trading in a distressed fashion and there is a lot of pain out there amongst retail and institutional investors alike. But fundamentals will matter when the dust clears. Let’s start with what caused the digital assets rally since October 2020:

1) Low rates / low dollar

- Still very much intact even though there are taper talks and inflationary data, as both rates and the dollar have not yet reacted, which is supportive of risk assets

2) Institutional money is entering the market

- Institutional money doesn't come faster or slower based on price moves. Those trying to deploy will still deploy, and many of them are. It is possible, however, that the declines in GBTC & COIN may have been leading indicators, as downward price movements demonstrate that institutional money was already slowing.

3) Elon Musk / Corporations

- The ESG narrative (which is just that, a narrative) is unlikely to ever go away at this point. Like a religion, no amount of science will change people's minds here, and this becomes more political theatre than substance. But Elon Musk's erratic tweets have brought ESG to center stage and this will likely give pause to corporates/institutional capital.

4) Strong Fundamental Growth and Usage

- DeFi, NFTs, Gaming and other types of digital assets are still seeing massive usage, and none of this was true the last time the market crashed over a year ago.

So you have 2.5 out of 4 factors that are still very bullish for risk assets, which means there still should be buying power on the sidelines. The question is just when and how it gets deployed. Those assets that cannot be valued (i.e. Bitcoin and most Layer-1 protocols) will be the hardest to have conviction on regarding price, but those that are asset-backed or have real cash flows (i.e. DeFi, CeFi, some NFT-platforms and sports/gaming platforms) in theory have valuations that are immune from a price shakeout. And investors will be looking for these greenshoots. For example, in March 2020, both Peloton (PTON) and Zoom (ZM) stocks got crushed in the first 3 weeks of the crisis, but the market soon realized that these were the types of companies that disproportionately benefit from a stay-at-home lockdown. Similarly, there will be certain areas of digital assets that disproportionately benefit from a coordinated government/regulatory attack on miners and exchanges:

- Miners in other jurisdictions, especially those with clean, renewable energy

- Censorship resistance storage / archiving (i.e. Arweave)

- Self-storage / wallets - free of centralized ownership

- Bitcoin, as a free-standing store of value and government resistant monetary asset

- And of course, DeFi, especially Decentralized Exchanges (DEXs)

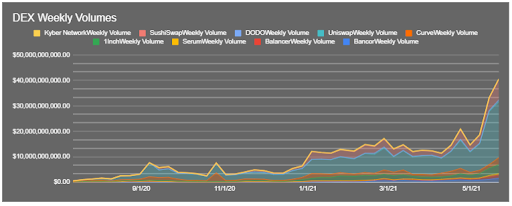

As Arca senior analyst, Alex Woodard, noted over the weekend in an internal update…. because of the market volatility, DEX trading volume continued its up trend with its highest volume week ever. This was led by Uniswap and SushiSwap which make up more than 70% of ETH total DEX volumes.

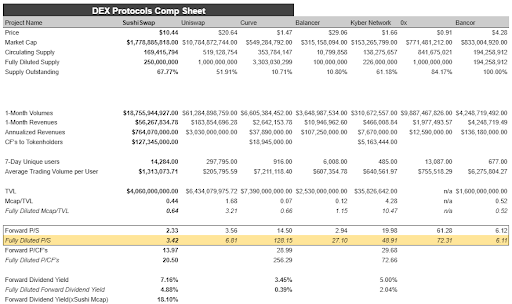

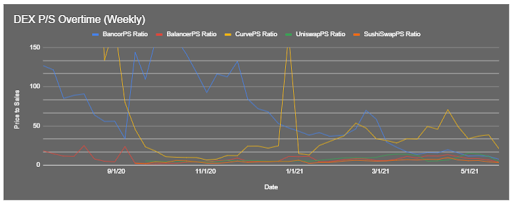

Overall the crash in the market has made DEXs increasingly attractive as metrics improve when volatility increases. The P/S metrics are the lowest they have ever been for almost all projects in the DEX sector.

Source: Arca Estimates

Source: Arca Estimates

It may take some time to heal these wounds, and regulatory risk is never going to completely go away, but this market will bounce back as it always has, though it’s likely that it will be other tokens besides Bitcoin that lead us back to all-time-highs.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

Source: Twitter / @marcomadness2

Source: Twitter / @marcomadness2